Quick Quiz: What Kind of Saver Are You?

Answer step by step. Your result will appear at the end.

A year is long enough to change your finances, but short enough to manage with a clear structure. That's the promise of the saving 52 week plan - a simple, time-boxed framework that turns small, scheduled deposits into a meaningful cash reserve by week fifty-two. Instead of relying on willpower, the plan leverages routine: you commit to a fixed cadence (weekly), a transparent rule for how much to set aside, and a visible way to track progress. The psychology is deliberate: frequent, bite-size wins build momentum; the calendar creates accountability; and the growing total provides continuous feedback. As coaches and planners know, those ingredients consistently outperform vague intentions to “save more this year.”

Equally important, a weekly challenge adapts to real life. You can start with cash envelopes or use a banking app; you can run the sequence forward (low amounts first) for quick early wins or backward (higher amounts first) while motivation is high.

You can smooth spikes by pre-funding rough weeks, and you can tie the finish line to a specific goal: an emergency buffer, a deductible, or a short-term purchase you'd rather cash-flow than finance.

The output is clear - steady behavior, measurable progress, and a pot of money large enough to matter. The inputs are clearer still - one rule, one schedule, and a plan you can execute in minutes each week.

Listen to the article - it is faster than reading!

What is the 52 Week Challenge?

The 52-week challenge is a structured savings routine that runs for one calendar year. Each week you set aside a specific amount, following a simple rule that escalates gradually. In the classic version, week 1 is $1, week 2 is $2, and so on until week 52 is $52. Those deposits add up to $1,378 by the end of the year. Many people flip the order - starting high and stepping down - to capture early momentum while motivation is strongest. Others keep the same total but even out cash flow by averaging amounts across pay periods. You can complete it with physical envelopes or digitally via sub-accounts or “pots.” The challenge works because it is concrete, transparent, and easy to audit at any point. It also builds a weekly money habit without complex budgeting. If a week is tight, you can swap amounts with another week and stay on track. The finish line is fixed, the rule is stable, and the progress is visible - three traits that make people actually finish. By week fifty-two, you've built both a savings balance and a repeatable system.

What is the 52 Week Rule?

The 52-week rule defines the structure that makes the savings challenge predictable and achievable. It's not just a countdown of weeks - it's the mathematical and behavioral framework behind how consistent micro-savings accumulate into meaningful results. The rule ensures that each week builds on the previous one, creating both a numerical progression and a psychological sense of growth. It removes ambiguity by replacing “save when possible” with a clear, scheduled obligation.

Because it operates on a fixed time horizon - 52 weeks - it balances discipline with flexibility: short enough to see results, long enough to form habits. It can also apply to benefits and financial planning, influencing how income or savings are evaluated over a year.

Below are the six key principles that make up the 52-week rule and explain its broader relevance.

-

Consistent Weekly Contributions

The foundation of the 52-week rule is simple: save a defined amount each week for one year. This cadence builds structure and accountability. Even if weekly deposits seem small, the cumulative effect creates exponential motivation - the more weeks you complete, the harder it becomes to quit. This frequency trains financial consistency, turning saving into a reflex rather than a decision. Over time, regular deposits rewire spending habits and strengthen confidence in meeting future financial goals. -

Incremental Progression

The challenge typically increases your contribution by $1 each week, starting from $1 and ending at $52. The gradual progression makes the plan psychologically accessible: it begins easy, builds comfort, and grows challenge as momentum develops. Unlike static savings goals, this rule introduces a sense of progression and accomplishment. Each week's deposit is proof of progress, making the journey motivating instead of monotonous. -

Fixed Duration (52 Weeks)

The one-year structure is deliberate. It aligns with budgeting cycles, seasonal spending, and tax years, making it easy to plan around life events. The time-bound nature ensures a clear finish line - long enough to see results but short enough to avoid burnout. A fixed duration gives participants measurable checkpoints and periodic reflection points for reviewing their growth and adapting future goals. -

Predictable Total Outcome

The rule produces a known final sum - $1,378 in the standard version. This predictability reinforces goal-setting and financial planning. Because the result is guaranteed if the schedule is followed, it builds trust in the process. Predictable outcomes help people visualize tangible rewards, whether that's paying down debt, funding a trip, or building an emergency buffer. -

Behavioral Conditioning

The repetitive nature of the rule is designed to strengthen saving as a habit. By committing to a manageable schedule, you replace impulsive spending with structured saving. Each successful week rewards self-discipline, reinforcing intrinsic motivation. The rule acts as behavioral training for long-term money management beyond the challenge itself. -

Broader Financial Application

The 52-week rule is also used in benefits and welfare contexts, particularly in determining eligibility or continuity of payments. It can measure consistent employment, savings accumulation, or income levels over a year. Understanding it helps individuals manage timing and compliance within financial systems. Thus, the rule serves not only as a savings structure but also as a framework for evaluating stability and progress across different financial domains.

Why the Saving 52 Week Plan Works?

The saving 52 week plan succeeds because it blends simplicity, habit formation, and visible results. Its power lies in predictability - every week is planned, every deposit builds confidence, and every milestone brings tangible proof of progress. Unlike abstract financial advice, this method gives immediate feedback, making it easier to stay motivated. It's flexible enough for any budget but structured enough to prevent procrastination. The plan also leverages behavioral psychology: consistent small wins create lasting motivation, while the linear structure reduces decision fatigue.

Below are five reasons experts consider it one of the most effective short-term saving frameworks available today.

-

Simplicity and Transparency

The plan is easy to understand and implement. You don't need complex apps, calculations, or tracking tools - just a clear weekly schedule. This simplicity makes it accessible to beginners while still effective for seasoned savers. The visible, transparent growth keeps motivation high and accountability strong, ensuring users can see results from week one. -

Habit Formation Through Repetition

Weekly repetition conditions behavior. Over time, your brain begins to treat saving as a natural, expected action rather than a chore. This consistency is crucial because personal finance success depends more on discipline than income. By week 52, the challenge has trained your mindset to prioritize saving automatically. -

Psychological Motivation

The ascending savings pattern is designed to create emotional momentum. The early stages are effortless, which builds confidence. As contributions increase, you feel more invested in the process, making it harder to abandon. That growing sense of achievement fuels long-term commitment - critical for maintaining financial goals beyond the challenge. -

Flexibility and Adaptability

Despite its structure, the plan can adapt to your situation. You can reverse the order, freeze high-payment weeks, or pool funds biweekly if that fits your cash flow better. This flexibility ensures sustainability without breaking the challenge's integrity. It meets you where you are, not where theory says you should be. -

Visible, Measurable Results

Each week's total acts as proof of progress. Seeing the number grow reinforces the belief that consistent action leads to real financial stability. This visibility transforms abstract goals into quantifiable achievements. By the final week, the proof isn't just in the balance - it's in the habit and confidence you've built.

What Happens After the 52-Week Period Ends?

After completing the 52-week period, most participants find themselves not only richer by $1,378 but also more disciplined and financially aware. The challenge's end isn't the finish line - it's a transition point. Many use the accumulated savings to fund short-term goals such as emergency funds, debt repayments, or vacations. Others roll the challenge forward, doubling contributions for the next year or setting a new target like $2,000 or $5,000. Psychologically, the completion reinforces the idea that small, structured habits lead to major outcomes, encouraging participants to expand their financial planning into budgeting, investing, or long-term goal setting.

If the challenge was part of a household effort, it often inspires collective financial behavior - families continue tracking expenses together or gamify new money-saving targets. The final step is reflection: analyzing what worked, identifying friction points, and adjusting for the next savings cycle. In essence, the end of 52 weeks marks the beginning of a lifelong habit of consistent, intentional saving.

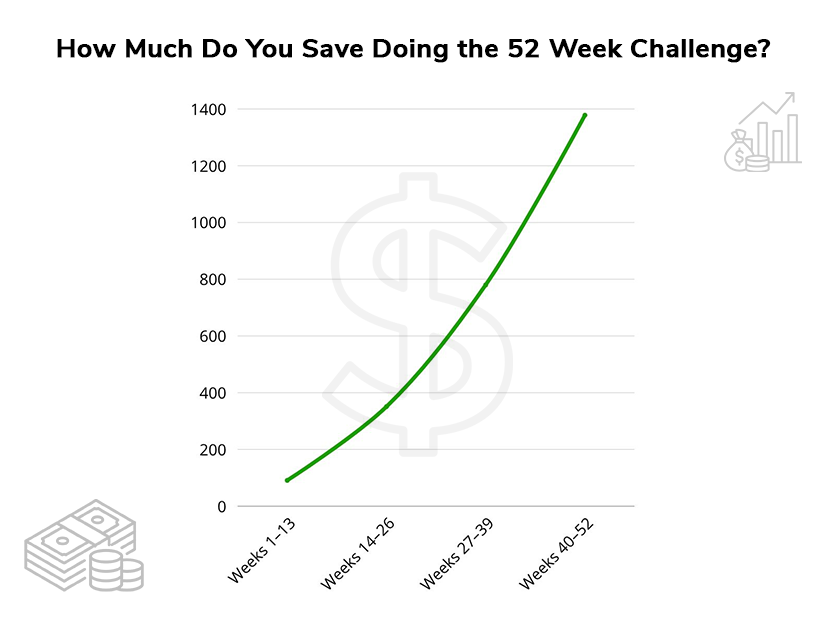

How Much Do You Save Doing the 52 Week Challenge?

The classic 52-week money challenge results in $1,378 saved by the end of the year. It's based on a straightforward formula: save $1 in week one, $2 in week two, and continue increasing by one dollar each week until week fifty-two, when you deposit $52. The total comes from adding all weekly amounts together (1 + 2 + 3 + ... + 52), which equals $1,378. What makes this total powerful is not the number itself, but the behavioral consistency it represents - the ability to stay disciplined for a full year. Financial planners often highlight this method as one of the simplest ways to build an emergency fund or a short-term financial buffer.

According to the Consumer Financial Protection Bureau (CFPB) and America Saves, micro-saving strategies like weekly incremental deposits significantly improve savings retention rates and financial stability among U.S. households (source). The $1,378 target can also be customized - doubling the weekly increments results in $2,756, while halving them yields $689. Regardless of the scale, the underlying principle remains identical: structured, repeatable deposits build meaningful savings faster than spontaneous attempts. The real value of the challenge lies in the confidence it gives people to manage cash flow intentionally over time.

How to Calculate the 52-Week Rule for Your Benefits?

The 52-week rule in the context of benefits or personal savings is a systematic way to measure consistent financial activity over one calendar year. For savings, it means tracking and compounding weekly deposits; for benefits, it refers to how continuous savings or employment affect eligibility or calculations over a 52-week period. To calculate savings, you simply add the weekly contribution to the cumulative total from previous weeks. The pattern is linear yet motivational because each addition visibly grows your total.

Below is a breakdown of how the 52-week money challenge accumulates from week one to week fifty-two.

52-Week Money Challenge Table

Quarter 1 - Building the Habit (Weeks 1-13)

| Week | Amount to Save ($) | Total Saved ($) | Example Use | Motivation Tip |

| Week 1 | $1 | $1 | Skip one coffee and start fresh | Small beginnings create strong financial habits |

| Week 2 | $2 | $3 | Bring lunch instead of eating out | Progress is proof that consistency works |

| Week 3 | $3 | $6 | Cancel one unused subscription | Every dollar saved builds long-term discipline |

| Week 4 | $4 | $10 | Prepare homemade meals this week | Saving small today grows big over time |

| Week 5 | $5 | $15 | Walk instead of paying for parking | Focus on progress, not perfection - keep going |

| Week 6 | $6 | $21 | Make your own morning coffee | Building control is more valuable than comfort |

| Week 7 | $7 | $28 | Limit online shopping impulse buys | Consistency beats intensity in money growth |

| Week 8 | $8 | $36 | Use coupons for groceries | Stay patient - slow progress compounds fast |

| Week 9 | $9 | $45 | Skip one streaming movie rental | Tiny cuts in spending create lasting change |

| Week 10 | $10 | $55 | Cook dinner at home twice this week | You're proving to yourself what's possible |

| Week 11 | $11 | $66 | Pack snacks for work or travel | Every intentional choice brings you closer |

| Week 12 | $12 | $78 | Choose generic over name-brand items | Replace spending impulses with saving wins |

| Week 13 | $13 | $91 | Sell one unused household item | You've completed 25% - celebrate progress smartly! |

Quarter 2 - Building Momentum (Weeks 14-26)

| Week | Amount to Save ($) | Total Saved ($) | Example Use | Motivation Tip |

| Week 14 | $14 | $105 | Replace takeout with a homemade meal plan | Stay focused - habits now drive automatic progress |

| Week 15 | $15 | $120 | Skip weekend entertainment spending | Every skipped purchase funds your future freedom |

| Week 16 | $16 | $136 | Avoid impulse Amazon buys | Your growing total is real momentum - stay on track |

| Week 17 | $17 | $153 | Share a meal instead of dining alone | Saving smart is self-respect in action |

| Week 18 | $18 | $171 | Try a “no-spend” day this week | You're controlling money - not the other way around |

| Week 19 | $19 | $190 | Cut back on premium subscriptions | Clarity, not luck, makes your savings grow |

| Week 20 | $20 | $210 | Do a home workout instead of gym visit | Financial strength mirrors personal discipline daily |

| Week 21 | $21 | $231 | Use loyalty rewards for groceries | Each conscious action multiplies your financial results |

| Week 22 | $22 | $253 | Prepare lunches for the week | You've turned saving into a predictable skill |

| Week 23 | $23 | $276 | Avoid unnecessary in-app purchases | You're halfway there - keep momentum strong |

| Week 24 | $24 | $300 | Batch errands to save gas | Consistency here builds peace of mind later |

| Week 25 | $25 | $325 | DIY a home maintenance task | You now think like a long-term wealth builder |

| Week 26 | $26 | $351 | Skip takeout coffee for a week | Halfway done - your discipline is now automatic! |

Quarter 3 - Strengthening Consistency (Weeks 27-39)

| Week | Amount to Save ($) | Total Saved ($) | Example Use | Motivation Tip |

| Week 27 | $27 | $378 | Review monthly subscriptions again | Systems, not motivation, make saving effortless |

| Week 28 | $28 | $406 | Cancel one unnecessary delivery app | You're turning awareness into financial control |

| Week 29 | $29 | $435 | Buy bulk groceries for the month | Think of every dollar as a silent worker for you |

| Week 30 | $30 | $465 | Skip one paid outing this week | The habit is stronger than the temptation now |

| Week 31 | $31 | $496 | Sell unused tech or gadgets | You're mastering financial choices that last forever |

| Week 32 | $32 | $528 | Borrow books instead of buying | The small actions are shaping your future comfort |

| Week 33 | $33 | $561 | Reduce thermostat use slightly | Comfort is temporary - stability lasts longer |

| Week 34 | $34 | $595 | Plan meals from your pantry | Your progress shows how powerful planning is |

| Week 35 | $35 | $630 | Switch one bill to autopay discount | Financial consistency equals personal confidence growth |

| Week 36 | $36 | $666 | Use cashback for savings deposit | You're learning to redirect every dollar smartly |

| Week 37 | $37 | $703 | Avoid weekend shopping trips | Keep saving - you're closer than you realize |

| Week 38 | $38 | $741 | Bring lunch on all workdays | You've built a lifestyle, not a limitation |

| Week 39 | $39 | $780 | Review savings goals and adjust | This is progress few people sustain - well done! |

Quarter 4 - Completing the Challenge (Weeks 40-52)

| Week | Amount to Save ($) | Total Saved ($) | Example Use | Motivation Tip |

| Week 40 | $40 | $820 | Cut dining out entirely this week | You're entering mastery - finish what you started strong |

| Week 41 | $41 | $861 | Plan next year's saving goal | You're saving automatically - your mindset has shifted |

| Week 42 | $42 | $903 | Skip a shopping trip altogether | Your effort now defines your financial future |

| Week 43 | $43 | $946 | Use coupons or cashbacks smartly | You're not just saving - you're compounding control |

| Week 44 | $44 | $990 | Batch cook and freeze meals | Efficiency is now part of your lifestyle habit |

| Week 45 | $45 | $1,035 | Recycle old items for extra cash | Smart savers think creatively, not restrictively |

| Week 46 | $46 | $1,081 | Skip one convenience service | You've proven financial consistency is a learned skill |

| Week 47 | $47 | $1,128 | Complete a week of no-spend challenge | You're financially stronger than you were 11 months ago |

| Week 48 | $48 | $1,176 | Avoid impulse online shopping | Each week of effort builds your long-term comfort |

| Week 49 | $49 | $1,225 | Use a cashback credit card wisely | This final stretch proves sustainable habits work |

| Week 50 | $50 | $1,275 | Review your financial year results | The finish line is near - your growth is visible |

| Week 51 | $51 | $1,326 | Decide your post-challenge savings goal | You've created a self-sustaining financial discipline |

| Week 52 | $52 | $1,378 | Celebrate your achievement responsibly | You didn't just save - you rewired your money mindset |

By the end of week 52, you'll have accumulated $1,378 - a sum achieved entirely through small, manageable steps. This table demonstrates not just arithmetic growth, but also the compounding effect of consistent habits - proving that financial progress depends on repetition, not complexity.

Best Strategies for Customizing the 52-Week Savings Plan

The beauty of the 52-week savings method lies in its flexibility. While the original version builds from $1 to $52, experts emphasize that the framework can (and should) be adjusted to fit different income levels, cash flow patterns, or personal goals. Customization keeps the plan realistic and sustainable - the key to finishing all 52 weeks without losing motivation. Whether you're managing irregular income, starting late in the year, or saving for a higher goal, there are proven ways to tailor the challenge without breaking its structure. Below are four professional strategies to help you adapt this plan while keeping your results measurable, achievable, and motivating - the best saving advice 52 week challenge experts can offer.

Reverse the Order for Immediate Wins

$1,378 savings base

Financial coaches often recommend starting from the largest amount and working downward. This “reverse challenge” means you begin with $52 in week one and finish with $1 in week fifty-two. The psychological advantage is twofold: you make the most substantial contributions when motivation is at its peak, and your financial burden lightens near year-end when expenses often rise. This setup also maximizes early savings growth - by the end of week 13, you'll already have set aside $1,144 instead of just $91 in the traditional version. The early lump sum can even be transferred into a high-yield account to earn interest for the remainder of the challenge.

Benefits: Frontloads savings, builds early momentum, reduces stress during holidays, and provides earlier access to emergency cash if needed.

Customize Increments to Match Pay Cycles

Potential savings: $1,300-$2,000

For people paid biweekly or monthly, syncing the challenge with your paycheck can make it effortless. Instead of weekly deposits, group the total monthly equivalent and save it in one transaction. For instance, save $10 the first month, $20 the second, and so on - or use the total of four weeks per pay period. This reduces transaction fatigue and integrates saving into your budgeting rhythm. Automating deposits on payday ensures consistency and removes the emotional friction of choosing whether to save. You can also adjust the starting increment: $5, $10, or $15, depending on your comfort level.

Benefits: Simplifies scheduling, aligns with income flow, minimizes skipped weeks, and supports higher consistency among salaried workers.

Apply the “Multiplier Rule” to Accelerate Growth

Potential savings: $2,756-$5,000

To reach more ambitious financial goals, you can double or triple each weekly deposit. The formula remains identical - Week 1 = $2, Week 2 = $4, and so on - but the total doubles ($2,756) or triples ($4,134) accordingly. This approach works well for dual-income households or anyone saving for larger targets such as travel, tuition, or major purchases. It keeps the psychological simplicity of the challenge while raising the stakes. To stay sustainable, plan “pause” or “flex” weeks every quarter, where you maintain or slightly reduce your contribution to balance cash flow.

Benefits: Scalable structure for larger savings goals, boosts motivation through higher visible results, and allows goal-based customization.

Gamify the Process with Randomized Savings

Flexible range: $1-$52 weekly

For those who find structure monotonous, the random method turns saving into a motivational game. Write numbers 1-52 on envelopes or cards, shuffle them, and draw one each week - whatever number you pick, that's your deposit amount. The unpredictability keeps the challenge fun while maintaining the same $1,378 target. It also adds flexibility: if one week's budget is tight, choose a lower number and leave higher ones for stronger cash-flow weeks. Apps and spreadsheets can randomize selections for digital tracking.

Benefits: Keeps engagement high, reduces pressure on tight weeks, and creates a playful, goal-oriented mindset around saving.

How Can I Save $5,000 with the 52-Week Money Challenge?

Saving $5,000 within the 52-week framework requires scaling the plan strategically rather than starting from scratch. Financial advisors suggest combining structure, automation, and small behavioral adjustments to multiply your outcome while keeping the routine manageable. Instead of drastic increases, the focus is on optimization: slightly higher weekly amounts, paired with interest gains, cashback funnels, or expense reallocation. Here's how experts recommend expanding the traditional model to hit the $5,000 mark without strain.

-

Increase Weekly Base Amounts

Double or triple your initial deposits - start at $4 instead of $1 and end at $208 instead of $52. This progressive scaling maintains the challenge format but accelerates total growth to about $5,000. Even modest increases compound powerfully when sustained for 52 weeks. -

Redirect Existing Savings Leaks

Track minor recurring expenses (subscriptions, delivery fees, impulse buys) and redirect them to your challenge fund. Canceling two $10 subscriptions alone frees up over $1,000 a year. Redirected waste becomes intentional progress without increasing income. -

Automate and Compartmentalize Savings

Use automatic transfers or “sub-accounts” dedicated to the challenge. When money moves automatically after each paycheck, there's no decision fatigue or risk of skipping weeks. Automation is the cornerstone of long-term consistency. -

Leverage Cash-Back and Rewards Programs

Apply cashback from cards or reward apps directly to your savings account. Treat these bonuses as part of your weekly deposit. It's psychologically easier to save “found money” than to cut existing expenses. -

Combine Interest and Investment Returns

Place your challenge savings into a high-yield savings account or short-term certificate of deposit (CD). Even a 4-5% APY return adds meaningful bonus income. Reinvest that growth, and your challenge can exceed $5,000 effortlessly by year's end.

Common Mistakes and How to Avoid Them

Even simple systems falter without structure, and the 52-week challenge is no exception. Most drop-offs happen not for lack of cash, but for lack of planning, weak tracking, or rules that don't match real cash flow. Treat your plan like a training program: clear milestones, visible progress, and contingencies for off weeks. Build in automation where you can, and design friction for spending rather than saving. Finally, review quarterly - what gets measured gets improved. Use the guidance below to turn 52 week challenge money saving from a good intention into a completed, confidence-building result.

| Common mistake | How to avoid it (practical fix) |

|

Starting with enthusiasm but no system People begin on a high note, then life happens: a busy week, a missed deposit, and the habit unravels. Without a written plan, a calendar cadence, and a tracking artifact, the challenge competes - and loses - against day-to-day demands. Relying on memory or willpower guarantees inconsistency and makes progress invisible, which erodes motivation quickly. |

Operationalize the routine on day one. Create a single source of truth (spreadsheet, app, or envelope board) and pre-schedule 52 reminders. Automate transfers where possible (weekly or tied to payday) and use a visual progress tracker you update after each deposit. Set “make-up rules” in advance: if you miss a week, split the amount over the next two weeks. Establish monthly checkpoints to reconcile totals and celebrate milestones (weeks 13/26/39). A system makes the behavior default; motivation becomes a bonus, not a requirement. |

|

Choosing a deposit curve that doesn't fit cash flow The classic $1-$52 ramp looks neat, but higher amounts can collide with rent, holidays, or irregular income. The result is skipped weeks or credit-card “saves” that defeat the purpose. Misaligned pacing turns a helpful structure into pressure. |

Tailor the math to your money rhythm. If income is variable, reverse the order (high early, low later) or randomize weekly amounts from a 1-52 pool to match lean and strong weeks. Paid biweekly? Aggregate two weeks into one transfer. Anticipate spikes (holidays, insurance renewals) and pre-fund those weeks now. You can also apply a constant step (e.g., $15 every week) that still totals to your target. The goal is sustainability - same rules, better fit. |

|

Tracking only in your head (no visibility) When progress isn't visible, the brain discounts it. You forget wins, underestimate momentum, and overreact to small setbacks. Without a dashboard, you can't catch drift early or feel the satisfaction that keeps you engaged through week 30+. |

Make progress tangible and public (to yourself). Use a wall chart, app widgets, or color-coded envelopes so each completed week is obvious. Snapshot totals monthly and note what enabled success (e.g., subscription cut, cashback). If saving with a partner, share a live tracker to add accountability. Visibility creates a dopamine loop - finishing the week feels rewarding, which sustains adherence through the middle stretch where most people quit. |

|

Letting small leaks sabotage deposits Micro-spends - delivery fees, duplicate subscriptions, impulse buys - quietly compete with your weekly transfer. The challenge isn't “too hard”; the budget is too porous. Without redirecting leaks, you force savings to fight every purchase decision. |

Pre-route leak savings into the challenge. Audit the last 60-90 days for recurring low-value spends. Cancel or downgrade, then set an automatic transfer for the exact freed amount on the same day the charge used to hit. Use separate “spend” and “challenge” accounts to add friction to reversals. Channel card cashback and round-ups into the challenge pot. Now your environment funds the habit - no extra willpower required. |

|

All-or-nothing thinking after a miss One missed week becomes two, then abandonment. People treat a slip as failure rather than a data point. This perfectionism turns a year-long practice into a pass/fail test. |

Install recovery protocols. Define a Missed-Week Playbook: (1) split the missed amount over the next two to three weeks; (2) substitute a lower number from a future week and reshuffle the schedule; or (3) add a micro-deposit (e.g., $5/day for five days) as a make-good. Document the reason (cash flow, forgetfulness, one-off bill) and add a prevention tweak (new reminder, adjusted curve). Resilience - not perfection - finishes challenges. |

|

Ending at week 52 with no next step Without a post-challenge plan, funds get repurposed casually and the hard-won habit dissolves. The result: you restart from zero later, losing momentum and the compounding benefit of consistency. |

Pre-decide the “Week 53” plan. Two weeks before finishing, assign the money a job (emergency fund, debt payoff, short-term goal) and open the destination account if needed. Roll your cadence into a new track: a doubled challenge, a flat weekly auto-save, or a targeted sinking fund (travel, car maintenance). Schedule a 30-minute review: what worked, what dragged, and which rule to modify. Graduation into the next system protects both the balance and the behavior you built. |

Real Cases: How People Actually Completed the 52-Week Challenge

Digital Tools and Apps for Saving 52 Week Plan

Technology has made saving money simpler, faster, and more transparent than ever before. For anyone taking on the 52-week savings challenge, using the right app can turn the process from a manual routine into an automated system. These tools track your weekly deposits, send reminders, analyze spending, and even move money for you automatically. The key is finding the balance between simplicity and control - some apps are designed specifically for challenges, while others provide a full-picture view of your financial health. Whether you're a first-time saver or someone scaling toward bigger goals, digital tools help you stay consistent, measure progress, and avoid emotional spending. Below are six expert-approved apps that can help you complete your 52-week challenge successfully and even amplify your savings potential over time.

52 Weeks Money Challenge (Mobills) is built specifically for users running the 52-week challenge. It provides a visual tracker that displays your current week, goal, and total savings in real time. Mobills' 52 Weeks Money Challenge feature allows you to customize the starting amount, reverse the order, or create multipliers (like doubling each week's deposit). What makes it powerful is simplicity - you can start the challenge with just a few taps and get weekly notifications to stay on schedule. For visual learners, graphs and color-coded progress bars make success tangible. You can also export your data for long-term planning. The app is ideal for beginners who want a straightforward, motivational interface without unnecessary complexity.

Plum uses artificial intelligence to automate saving and investing. It connects directly to your bank, analyzes your spending behavior, and automatically transfers small amounts into savings or investment accounts. The app also offers a dedicated “52-week mode,” where deposits increase incrementally every week, just like the traditional challenge. What sets Plum apart is automation: once you activate the challenge, it quietly builds your balance without requiring manual input. You can adjust aggressiveness levels depending on your comfort zone. Additionally, Plum provides financial insights and optional investment portfolios, allowing you to grow your challenge savings through interest or market gains. It's ideal for those who prefer a “set it and forget it” approach.

YNAB (You Need A Budget) is designed for people who want total visibility over their finances while pursuing structured goals like the 52-week challenge. It allows you to assign every dollar a job, ensuring savings don't get lost in everyday spending. You can create a dedicated “52-Week Challenge” category within your budget, automate weekly transfers, and monitor how the challenge aligns with your broader financial picture. YNAB's biggest advantage is accountability: you'll always know where your money goes, when to adjust, and how your savings plan fits within your income and priorities. It's perfect for disciplined savers who want the challenge to integrate seamlessly into a long-term budgeting system.

Monarch Money provides a sleek, analytics-driven experience that blends budgeting, goal tracking, and financial planning into one platform. For the 52-week challenge, users can set custom recurring goals with target end dates, visual progress bars, and dynamic charts showing cumulative growth. Monarch links multiple accounts and offers real-time collaboration - making it excellent for couples or families doing the challenge together. You can tag deposits, categorize spending, and forecast how adjusting contributions will affect total savings. Beyond the challenge, Monarch helps manage investments, debts, and net worth. It's a premium option for users who want a strategic, data-informed approach to savings and household finance.

Goodbudget brings the envelope budgeting system into the digital age, which fits perfectly with the 52-week challenge format. You can create virtual “envelopes” labeled from 1 to 52 and allocate funds accordingly each week. The app syncs across devices, allowing partners or family members to participate collaboratively. Its transparency makes it ideal for households or anyone who prefers tangible visual feedback. The ability to analyze category-level spending ensures that your challenge contributions don't conflict with other financial goals. Goodbudget promotes intentional saving - you see exactly where your money is going and consciously choose to prioritize the challenge each week.

EveryDollar, developed by Ramsey Solutions, is a powerful yet simple budgeting app focused on goal-based saving. It lets you assign weekly or monthly contributions toward a specific fund like the 52-week challenge. You can track progress visually, receive alerts for missed weeks, and integrate the challenge with your broader financial plan. EveryDollar is built around the zero-based budgeting principle, ensuring that each dollar in your paycheck has a defined role - including savings. This structure prevents overspending and keeps your challenge deposits on track. The app's clean interface and customizable dashboards make it a favorite for users who value organization and clarity over complexity.

How to Choose the Right App?

Your choice depends on your needs and how you want to manage your money.

- For simplicity: If you just want to track the challenge with no bells and whistles, a dedicated 52-week challenge app like Mobills is your best bet.

- For automation: If you prefer to set it and forget it, an automation-focused app like Plum or Acorns will do the heavy lifting for you, analyzing your habits and moving small amounts automatically.

- For full financial oversight: If you want to integrate the challenge into a broader financial plan, use a professional budgeting tool like YNAB, Monarch, or Goodbudget to align your savings with income, bills, and goals.

Each of these apps supports the same principle - consistent, trackable progress - but their interfaces and features cater to different saving personalities. The key is consistency: whichever app you choose, commit to using it weekly, reviewing progress monthly, and celebrating milestones. That's what turns technology into transformation.

Conclusion

The 52-week challenge is more than a savings experiment - it's a behavioral framework that rewires how you think about money, structure, and accountability. It transforms saving from an abstract intention into a concrete, measurable process that builds momentum week after week. The real success lies not just in reaching $1,378 but in developing consistency, awareness, and emotional resilience toward financial planning. Each deposit reinforces that small actions, repeated systematically, can outperform large but inconsistent efforts. The challenge works because it's flexible enough to adapt to any lifestyle, yet structured enough to maintain discipline. Whether you're building your first emergency fund or strengthening an existing plan, this method provides a roadmap that's simple, motivational, and time-tested.

By the end of 52 weeks, you gain more than money - you gain control. The structure helps you prove that saving isn't about luck or income level; it's about repetition and mindset. Once completed, you can easily scale it: double the weekly amounts, link it to investment accounts, or reframe it as a family project. The ultimate takeaway is that financial growth follows behavior, not complexity. The 52-week challenge gives you both the numbers and the confidence to keep that growth going for years to come.

FAQ About the 52 Week Challenge

How to save $1,378 in 52 weeks?

The math behind the challenge is simple but powerful. You start by saving $1 in week one, $2 in week two, and continue increasing by one dollar each week until week fifty-two, when you deposit $52. The cumulative total equals $1,378 by the end of the year. You can reverse the order - starting from $52 and working downward - to build savings faster early on. Automation is the key: set recurring transfers from your bank or digital wallet to eliminate decision fatigue. Using apps like Mobills or Goodbudget ensures consistent tracking and motivation. If your budget allows, doubling the contribution schedule results in $2,756, while maintaining the same psychological framework. The point isn't the exact number but the system that makes saving predictable and repeatable over time.

How to effectively track your progress in a 52-week money challenge?

Tracking progress turns motivation into momentum. Start with a visual method - use a spreadsheet, printable tracker, or dedicated app where you check off each completed week. Digital tools like YNAB or EveryDollar integrate this directly into your budgeting system, showing cumulative totals and trend graphs. For physical saving, envelope systems or jars labeled with each week's number work just as well. The key is visibility: seeing progress keeps you emotionally connected to the outcome. Review your tracker monthly to identify skipped weeks or cash flow issues. Gamify the process by celebrating milestones (e.g., every $250 saved) and adjusting goals as confidence grows. The more transparent your progress, the higher your likelihood of finishing all 52 weeks successfully.

How to stay motivated during a year-long savings challenge?

Motivation often fades around the halfway mark, so the key is designing your environment for success. First, automate your transfers to remove the need for weekly willpower. Second, visualize your progress - use charts, trackers, or apps to keep the results tangible. Third, tie your savings to a meaningful goal such as travel, debt payoff, or an emergency cushion. Behavioral research shows that linking savings to purpose increases consistency by over 60%. Additionally, allow flexibility: if one week is difficult, swap it with a smaller deposit instead of quitting. Surround yourself with accountability - friends, partners, or online savings communities. Finally, reframe the challenge as proof of discipline, not deprivation - each week completed is a visible investment in your financial independence.

What happens if I miss a week during the 52-week challenge?

Missing a week doesn't mean failure - it's an opportunity to adjust and improve. The best approach is to create a recovery plan: split the missed amount over the next two to three weeks or replace it with a smaller deposit and make it up later. Flexibility ensures long-term success while keeping your motivation intact. If cash flow is tight, skip the next highest amount and substitute a lower one, ensuring your weekly routine continues. Many apps allow you to “mark” a skipped week and automatically reschedule it. The most important factor is consistency, not perfection. Missing one or two weeks won't derail your outcome if you stay engaged and resume the habit promptly.

What should I do with the money after completing the challenge?

Once you've completed the 52-week challenge, decide on a clear purpose for your accumulated funds before they blend back into your regular budget. Common uses include creating an emergency fund, paying off high-interest debt, investing in low-risk assets, or saving for a specific short-term goal like travel or tuition. Financial planners recommend keeping the momentum by immediately setting a new goal or starting a modified version of the challenge - perhaps doubling weekly contributions or extending it into an annual auto-transfer. You can also transfer the balance into a high-yield savings account to continue compounding growth. The key is to give your money direction so the habit remains intact, turning a one-year challenge into a lifetime of consistent saving behavior.

Scarlett Mitchell

Consumer Finance Journalist | Making Money Management Clear and Practical

Noah Bennett

Credit Score Specialist | Helps rebuild financial health through better credit management